Hey, it’s Spencer here. Dan and I worked on a trade idea with some fundamental analysis around Alibaba based on their earnings results. As always, feel free to hit us with any feedback!

One other logistics note: we’ll be switching email providers next week, so be sure to check your spam folder and other mailboxes for our content and add us to your contacts if you haven’t done so already. Onto BABA…

Amidst the news this week of Amazon (AMZN) CEO Jeff Bezos planning to step down in Q3 of this year, you may have missed some of the news coming out of the earnings of mega-cap tech peer and Chinese counterpart Alibaba (BABA).

Recently, BABA stock’s been struggling due to antitrust scrutiny over the proposed IPO of BABA’s Ant Financial Group. However, Bloomberg is reporting that BABA/Ant Financial has arrived at a restructuring plan with regulators, agreeing to turn Ant Financial into a bank holding company with more strict capital requirements. The IPO seems to be on hold for the foreseeable future, but importantly, a forced divestiture is likely to be averted.

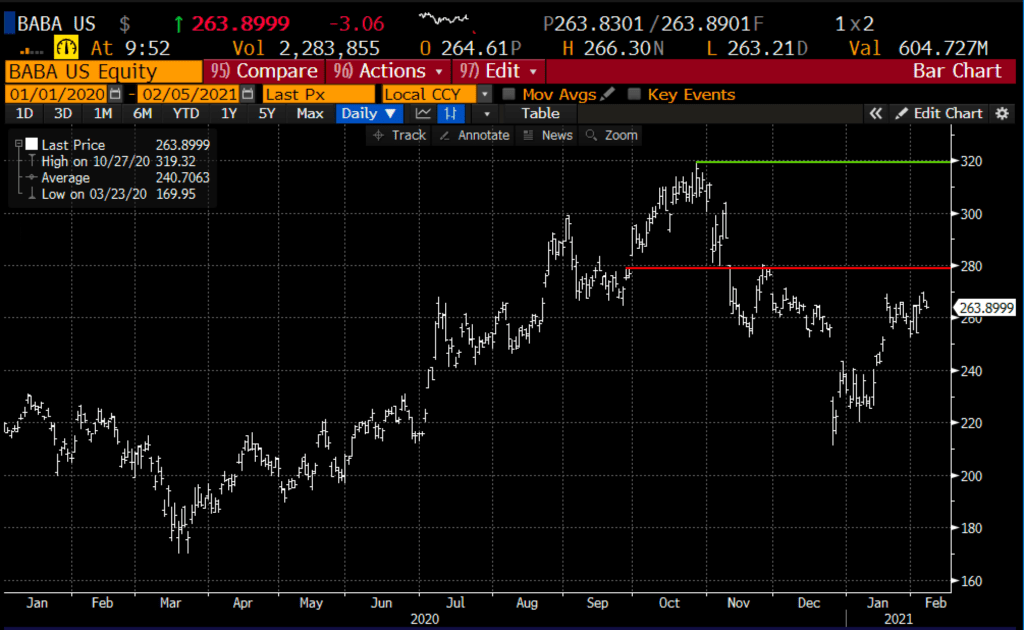

This is welcome news for BABA, jumping 3.5% Wednesday on the news. However, we’re still nearly 18% off from the all-time highs of nearly $320 that the stock reached in late October 2020. The stock found some support last month in and around its breakout level from last summer, and now sits between its 200-day moving average on the downside and its 100-day moving average on the upside:

Coming out of the earnings call, though, perhaps the most important piece of news was BABA reporting profitability in its cloud computing business for the first time in a single quarter.

Let’s put this in the context of some of this week’s news in US mega-cap tech. Jeff Bezos’s successor Andy Jassy currently heads up AMZN’s cloud unit AWS. Alphabet (GOOG) this week broke out their cloud business for the first time… and it wasn’t pretty, reporting a $5.61 billion loss on $13.06 billion in revenue in 2020. By contrast, in the same period, AWS represented just 12% ($45.4 billion) of Amazon’s revenue but a staggering 60% ($13.5 billion) of operating income for the company.

This underlies the importance of first-mover advantage, and, as China becomes more and more digitized, what is to come in the Chinese cloud market. In tapping their AWS chief, it also speaks to where Amazon sees sustained profitability coming from, emphasizing their incredibly high-margin cloud business over their original e-commerce business. With BABA also guiding that they expect their cloud division to become profitable within this current fiscal year, investors are (rightfully) excited about the prospects of an essentially unchallenged Chinese cloud market.

BABA’s core e-commerce business is still reliable, growing 38% year over year while delivering a 34% adjusted EBITDA margin and constituting 89% of the company’s revenue – high growth in spite of the fact that China is handling the pandemic and reopenings better than the US. Just as was the case with other mega-cap tech, it is reliable growth and margins like these in a core competency that allows for those successful “other bets” (as Google calls them): BABA’s cloud unit will soon join Amazon’s AWS, Google’s email/G-suite products and countless others as winning bets.

BABA is the cheapest place to get mega-cap tech exposure… but if the past few months’ headlines/regulatory fears are any indication, perhaps it deserves the lower multiple. Ultimately, however, I’d be a buyer of BABA long-term given the cloud business, the financial arm in Ant Group that looks increasingly unlikely to be spun out, and the power of scale in a largely-untapped Chinese market.

So what’s the trade?

For long-term investors looking to enter, BABA’s been volatile the past few weeks on these headlines but is positioned to go higher as this deal appears to be imminent, with the range we’re trading at now looking to be an attractive entry point.

For shorter-term traders looking to play this with options, I’d look to a bullish call spread targeting a few months out, which should be enough time to see how BABA’s Ant Group shakes out from a regulatory perspective and the gradual re-rating on the cloud business. Considering how volatile the stock has been, we can combine the fundamental story with the underlying volatility to come to a bullish view that we can express with options.

Bullish Trade Idea: BABA ($264) Buy April 265 – 320 call spread for ~$14

– Buy to open 1 April 265 call at ~$18

– Sell to open 1 April 320 call at ~$4

Breakeven on April expiration:

Profits of up to 41 between 279 and 320 with a max gain of 41 at 320 or higher

Losses of up to 14 between 265 and 279 with a max loss of 14 at or below 265

Rationale: This trade idea risks about ~5% of the stock price, breaks even up ~6%, has a max gain of up to $41 or ~16% of the stock price if the stock is up 21% on April expiration.

The trade idea targets a technical breakout above $280 which was an important technical resistance level back in November prior to the stock’s collapse on news of the pulled Ant Group IPO.

Why a call spread? Any continued bad news or pushout of Ant IPO, not to mention the risk of a market pullback and this stock is back below $240. For bulls in the name, we like defining our risk.